Ergodicity: Why Averages Kill Your Strategy

Imagine a wealthy eccentric walks into your boardroom and offers your executive team a game.

He places a revolver on the table. It has six chambers and one bullet. He says, "If you pull the trigger and survive, I will give your company $10 million. If you lose, your company goes bankrupt."

Your Chief Financial Officer immediately runs a standard Expected Value (EV) calculation. "There is an 83.3% chance of winning $10 million, and a 16.7% chance of losing everything," the CFO says. "On average, the expected return of playing this game is highly positive. Mathematically, we should play."

If you listen to your CFO, your company will eventually die.

The CFO has made a catastrophic mathematical error. They have confused ensemble probability with time probability. They are assuming the world is Ergodic. It is not.

Understanding the concept of Ergodicity is the ultimate litmus test for the Chief Wise Officer. It explains why managing a company based on "average returns" will inevitably lead to total ruin.

The Illusion of the Ensemble

To understand Ergodicity, we must look at how statistics deceive us.

An Ergodic system is one where the average outcome of a group of people playing a game once is exactly the same as the average outcome of one person playing the game repeatedly over time.

A casino roulette table is mostly ergodic. The casino's edge is the same whether 100 people play one spin, or one person plays 100 spins.

But business, life, and the Russian Roulette game above are Non-Ergodic.

- The Ensemble Average: If 100 different CEOs play the Russian Roulette game once, 83 of them will win $10 million, and 17 will go bankrupt. The average payout for the group is fantastic.

- The Time Average: If you (one single CEO) play that same game 100 times in a row, your chance of survival drops to zero. You will hit the bullet.

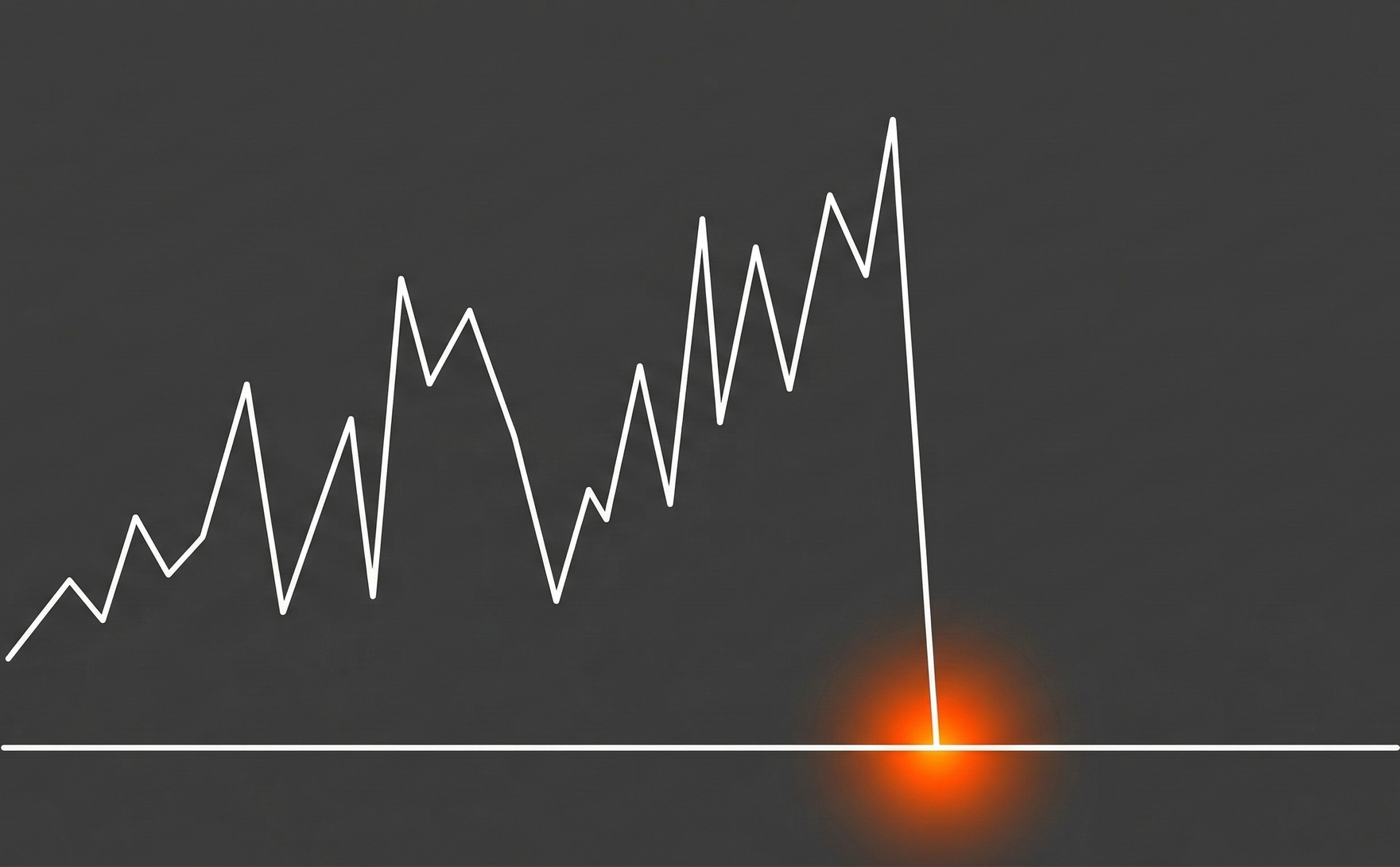

The CFO's spreadsheet calculated the "Ensemble Average" (what happens to a theoretical group of companies). But you are not a theoretical group. You are a single entity moving through time. And in a non-ergodic system, there is an Absorbing Barrier, a point of ruin from which you cannot recover. Once you hit bankruptcy, the game is over. You do not get to participate in the "average" future returns.

As Nassim Taleb famously summarized: "Never cross a river that is, on average, four feet deep."

How Averages Kill Corporate Strategy

Modern business is obsessed with Expected Value and average returns. We optimize our strategies for the highest average ROI. But by ignoring the risk of the absorbing barrier, we build fragile companies.

1. The "Average" Customer Does Not Exist Retailers often design store layouts and product lines for the "average shopper." But if half your customers are hyper-budget-conscious college students, and the other half are luxury-seeking executives, the mathematical "average" is a middle-class shopper who doesn't actually exist. By optimizing for the average, you alienate your actual, distinct customer bases.

2. The Debt Trap (Leverage) Why do highly profitable, successful companies suddenly go bankrupt during a minor recession? Because they over-leveraged based on average historical returns. They borrowed millions because, on average, their return on capital exceeded the interest rate. But leverage pushes you closer to the absorbing barrier. A single bad quarter (a Black Swan) hits the barrier, the bank calls the loan, and the game is over. The "average" 10-year return no longer matters because you didn't survive year three.

3. The Myth of the "Acceptable Risk" In non-ergodic environments, any strategy that carries a risk of total ruin, no matter how mathematically small, is an unacceptable strategy. If a new product launch requires you to bet the entire payroll of the company, it doesn't matter if the market research shows a 95% chance of success. If you run that strategy enough times, the 5% will inevitably hit, and the company will die.

The CWO Strategy: Survival First

The Chief Wise Officer does not manage for maximum average return. They manage for compounding survival.

1. Respect the Absorbing Barrier Before analyzing the potential upside of any strategic move, identify the absorbing barrier. What is the absolute worst-case scenario? Does this decision carry a risk, however small, of bankrupting the company, destroying the core brand reputation, or violating the law? If the answer is yes, you do not take the bet. Period.

2. Optimize for "Time Average" Stop asking, "What is the expected ROI of this project?" Start asking, "If our specific company made bets exactly like this sequentially over the next ten years, would we survive the inevitable strings of bad luck?" You must ensure that you can stay in the game long enough for the law of large numbers to actually work in your favor.

Conclusion: Stay in the Game

Warren Buffett’s two rules of investing are:

- Never lose money.

- Never forget rule No. 1.

People think this is just folksy billionaire wisdom. It is not. It is a brilliant, rigorous application of non-ergodic mathematics. Buffett understands that to reap the rewards of compounding interest over time, you must absolutely eliminate the risk of hitting zero.

Averages are a trap for the foolish. Do not let your spreadsheets convince you to play Russian Roulette. The only strategy that matters is the one that guarantees you are still sitting at the table tomorrow.

No spam, no sharing to third party. Only you and me.

Member discussion